Sui's Decentralization: A Forgotten Cause?

Mar 26, 2025

Max Sherwood

I. Introduction

Sui’s rise from a mothballed project at Facebook to one of the leading L1 blockchains is an example of the rapid success that’s possible in crypto. Mysten Labs and the Sui Foundation seem to have executed flawlessly on the L1 playbook. Yet, there is room for improvement for Sui’s network and staking ecosystem.

There’s no doubt that Sui’s yardstick is Solana, a chain with several years of head-start but very similar value propositions to the crypto industry: cheaper transactions and an easier developer experience.

However, as Solana spent years struggling against significant narrative headwinds, with non-stop accusations of financial and infrastructure centralization, Sui seems to have emerged relatively unbothered. Ironically, Sui does in fact face some of these challenges, arguably more so than Solana, even 2 years after the launch of its mainnet.

At H2O Nodes we are bullish on Sui and invested in the success of its ecosystem, as a validator on Sui and Walrus. We also believe that decentralization is a journey that never ends. In that spirit, with this report I will seek to shine a light on the successes and areas for improvement of Sui’s blockchain network at this point in time.

Sign up to our newsletter to keep up to date with the latest from H2O Nodes.

II. Validator Network Decentralization

I’m no data scientist, but thanks to validator.wtf by the Suiet wallet team, I can easily see the locations and hosting providers used by Sui’s mainnet validators. I’ve visualized the data below, which shows the breakdown of validators by number, without taking into account their stake. (Although stake distribution is important, it’s much easier to migrate stake from one validator to another than it is to migrate a validator from one location to another.) So, let’s dive in.

Hosting Providers

Sui’s validators utilize 36 hosting providers. I’ve definitely seen worse, and I feel relieved seeing Latitude.sh in the number one spot. They are a crypto-friendly provider, long having served the Solana validator market with great success. Not only that, but as a Brazil-based company they offer hardware locations across South America and the globe, enabling validators to meaningfully contribute to geographic decentralization. (That’s in stark contrast to Hetzner, who prohibits crypto-related services in their terms of service and was responsible for the shut-down of 20% of Solana’s validators in a single day back in 2022. #neverforget. Only one Sui validator currently uses Hetzner.)

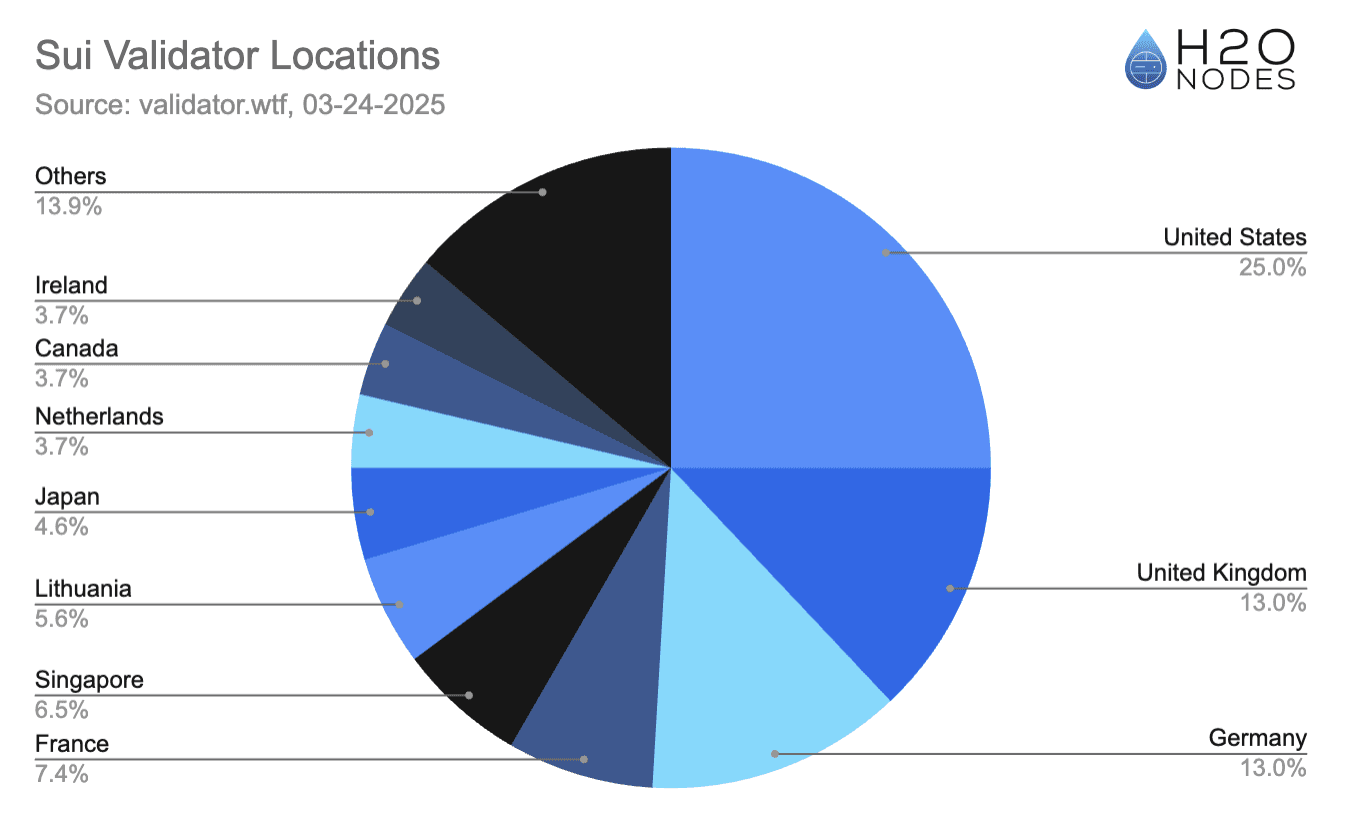

Validator Locations

Validator locations leave a bit more to be desired. With over half of the network’s validators located in three countries, it’s not inconceivable that the network could suffer real effects from an interruption in under-sea cables, a sudden change in regulatory stance, or something entirely unpredictable. However, the total of 22 countries is good.

Overall, from what I’ve seen on other networks, I would say that Sui’s validator network is no more or less centralized than is typical.

Operators tend to gravitate toward the most reliable, best connected, and least expensive bare metal providers, which are typically located in the US and Germany. Without any incentive to disperse geographically, operators are unlikely to move, and will experience lower latencies the closer they are to other operators, creating a crisis of the commons. However, as long as further centralization does not occur, I wouldn’t say that this is a cause for concern at the moment. Maybe I’ll do this report again in a year’s time and see if there are any discernable trends.

Barriers to Entry

Sui is another data-center-only chain, with hardware requirements high enough to rule out anyone operating a performant validator from home. (Unless someone has a sick home lab setup…) But while I’ve heard Solana take flak for the high cost of a server, I haven’t heard nearly as much criticism of Sui. (Perhaps it's just not on the radar of the Ethereum maxis? Or they don’t feel threatened to the same degree?)

The minimum hardware requirements specified in the documentation are: a CPU with 24 physical cores, 128 GB of memory, 4 TB of NVME storage, and 1 Gbps network capacity. Definitely well past high-end gaming PC territory and in the low to mid-range server market, costing easily $5k - $10k. (or, for rent for perhaps $500-$1000/month. Quite the commitment)

But the real barrier to entry for Sui validators is not the cost of hardware, it’s the minimum required stake. A Sui validator needs 30M SUI of stake to join the validator set, (over $50M at the time of writing). A validator is removed if they have less than 20M Sui for one week, or less than 15M SUI for 1 day. Keeping in mind that many validators have the majority of their stake coming from the Foundation, this is probably the largest centralization vector of the Sui chain. (FUDers, take note…)

Obviously, it’s not in the interest of the Foundation to reduce the number of active validators on the network, but the fact that they have this power over many of the validators is spooky. Even reports like this one, for example, create risks for my validator business if I rail too strongly against the Foundation. What’s the solution? Broader distribution of stake, from independent actors. That, however, is a token distribution problem, which brings us to the next section.

III. Stake centralization

With 5% of total supply circulating at launch, Sui’s tokenomics were questionable at best, but now going on two years after mainnet launch, the picture has improved, as more tokens have unlocked and changes hands on public marketplaces.

As stated on their blog, Sui explained:

Over 50% of SUI tokens are in the Community Reserve which is initially managed by the Sui Foundation. These tokens will be distributed to builders, researchers, validators, and other network participants through a variety of programs, including the Developer Grant Program, which awards tokens to early projects building on Sui, and the Delegation Program which provides tokens to validators that can’t meet the upfront costs of operating on the network. Most of the other 50% of SUI is allocated to early contributors to and supporters of the network.

Another way of saying this, is that the entire allocation of Sui is either in control of the Foundation or the investors at launch. The public gains access to tokens as they unlock and are sold to the public on exchanges, given out by Foundation as part of grants and community programs and earned by validators. So, until a significant portion of the tokens are unlocked, sold, and/or distributed by Foundation, there is little hope of real independent stake to support validators on the network.

CoinMarketCap tells me that 3.16B of the total supply of 10B SUI tokens have unlocked, so, for the moment, I’m going to assume that most validators still receive the majority of their stake from the Foundation, as independent stake slowly becomes more significant. (Does anyone out there have the time, skills, and bravery to do a deeper analysis?)

Stake Distribution

Network | Nakamoto Coefficent |

Sui | 18 |

Solana | 20 |

Aptos | 18 |

Near | 12 |

Celestia | 6 |

While the previous section reads fairly bearish, I should state that the Foundation actually deserves praise for the way they bootstrapped the network at launch, distributing stake across an initial set of 100 validators.

In my opinion, once tokenomics allocations are set, a Foundation has a responsibility to delegate its tokens across as many validators as possible to ensure the decentralization of the network. Sui Foundation did just that, and with over 100 validators active on the network, the network now has a Nakamoto coefficient of 18, which is very reasonable compared to other networks. Keep in mind other networks like Hyperliquid, which recently launched with a mere 16 validators, 5 of which were run by the Foundation. Aleo also comes to mind, which also launched with 16. The situation on Sui could be much worse.

The biggest thorn in the side of Sui’s Nakamoto coefficient are the two most highly staked validators, both run by Mysten Labs, which together have around 5.8% of stake. Sure, it’s good for the labs entity to gather experience running a validator, but this looks primarily like a way of generating revenue for the labs entity. Perhaps there would have been a more elegant solution to finance the labs entity off-chain, while allowing them to run lower-stake validators which don’t compromise the decentralization of the chain?

The distribution of stake across all validators is fairly lopsided, but does not exhibit the extreme long-tail demonstrated by Solana’s stake distribution. One interesting insight is how many validators have almost exactly the same level of stake, which supports the thesis that Foundation delegations are a primary source of stake for the majority of validators.

Looking at the percentage of network stake per validator, I am reminded of Lido’s goal to limit stake per operator to 1%. We all know how much heat they’ve taken, so seeing operators on Sui with well over 1% of stake is a bit unsettling. However, this isn’t an immediate cause for concern for the health of the network, it just lowers the Nakamoto coefficient - the number of operators who would have to collude to compromise the network.

Token Supply Inflation

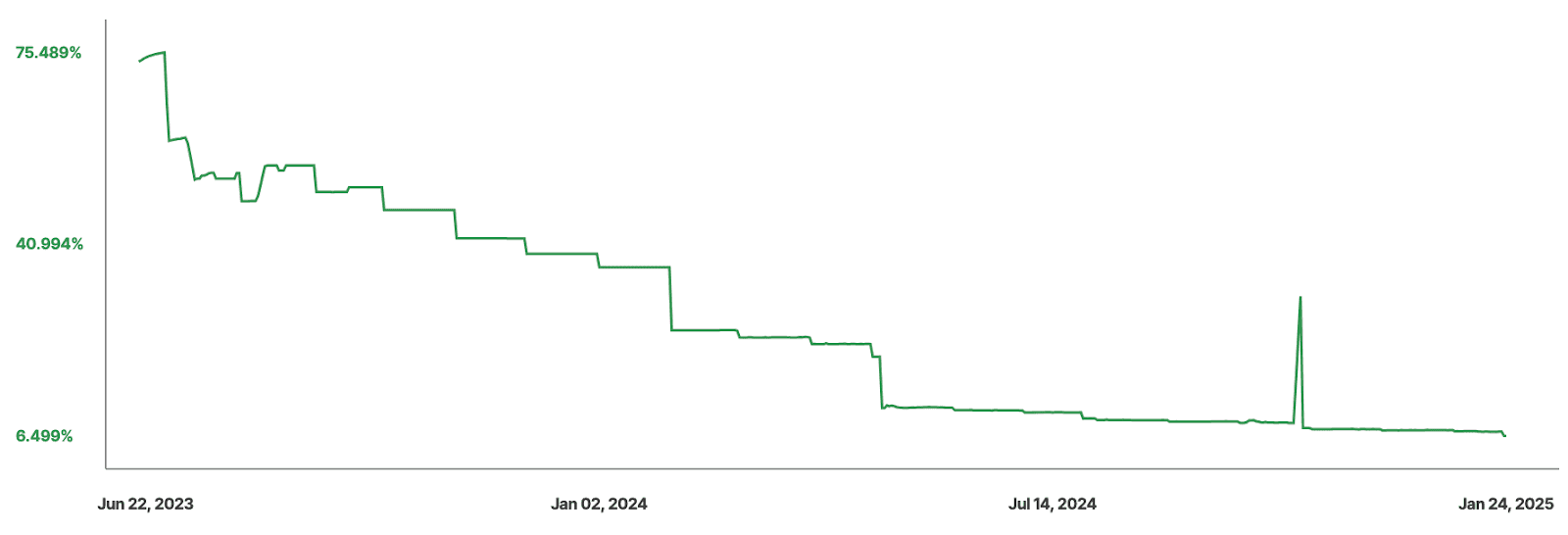

Another area where praise is due: Mysten Labs clearly put careful consideration into Sui’s token unlock and inflation schedules. Despite launching with a tiny 5% of circulating supply, due to relatively low staking APY, token unlocks were not brutally combined with high inflation. Shown below in the charts from Staking Rewards, as the staking APY (blue) decreased from 4.5% to 2.5%, token inflation (green) reduced to 6.5%. This is in line with the Sui protocol reduced inflation by 10% every quarter. (I couldn’t find official Sui communications regarding this… maybe it’s hidden in the whitepaper?)

Is 2.5% APY enough to attract stakers and maintain economic security for the network? Well, with 77% of the supply staked, it seems not to matter. This may be another sign of the dominance of the Foundation’s token holdings, but with a staking market cap near $20B, Sui’s economic security is solid. However, I do imagine it’s possible that the staking rate will fall as tokens make their way into the hands of the public, who aren't motivated to stake at such a low APY. Although, perhaps this will assist in the growth of liquid staking, where users can stake their SUI but still use liquid staked tokens in DeFi? Only time will tell.

IV. Mainnet Stability

Putting it all together - how has mainnet performed?

With only one instance of mainnet downtime in the two years since launch, Sui has avoided the toxic association with downtime that’s plagued Solana’s reputation. The single outage on 21 Nov 2024 lasted for only 1 hour and 6 mins, fixed by a release from the team which was quickly implemented by the operators.

Sui Foundation published a post mortem blog article the same day, which explained the cause of the bug and outlined what they would do to avoid a similar situation in the future. Let’s see how long Sui can keep going without another hiccup, but one mainnet outage in two years is already an improvement on Solana, which sadly still hasn’t gone an entire year without an outage in its 5 years of operation.

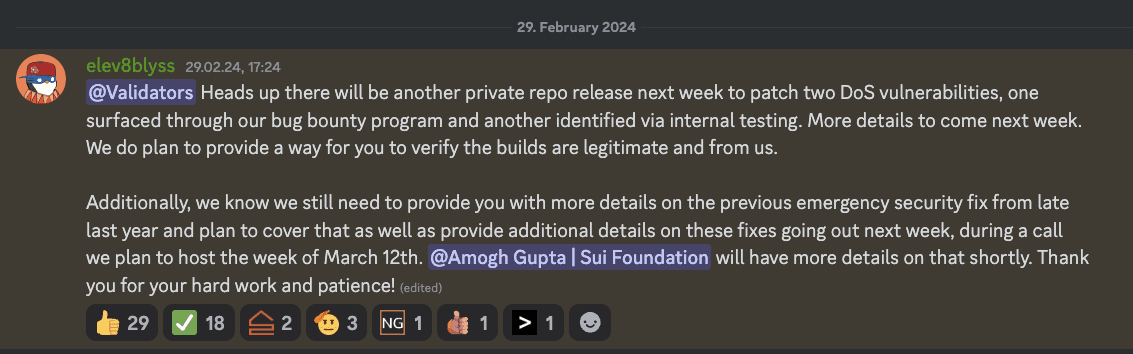

Bugs & Emergency Releases

Of course, urgent patches are quietly pushed out to operators every so often, but no major vulnerabilities have been exploited to date, and the Mysten Labs team has been professional in their overall handling of these. See below an example of the communications we received when a vulnerability was discovered, which in this instance discovered via a bug bounty and not an urgent emergency release.

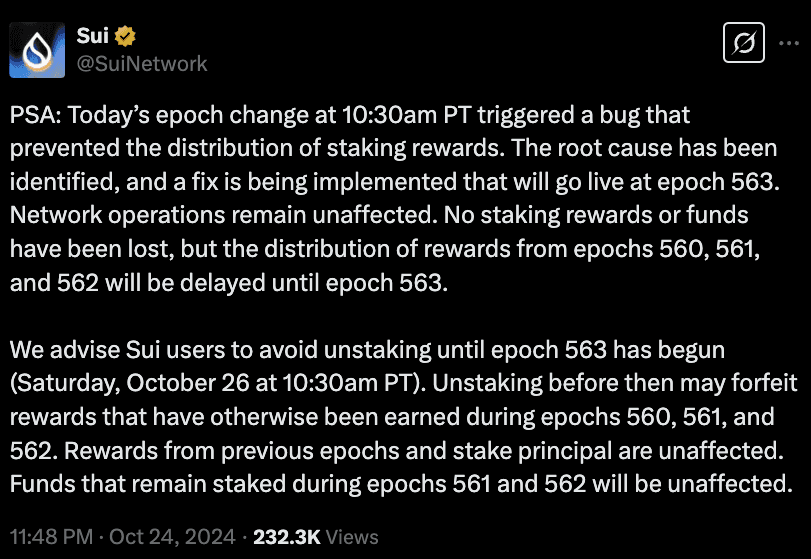

The only major bug that comes to mind is the lack of staking reward distributions in epochs 560, 561, and 562 that had to be compensated for in epoch 563. (This is what caused the glitch in the APY and inflation charts we saw earlier.) This too, was handled with transparent and professional communications, as shown below.

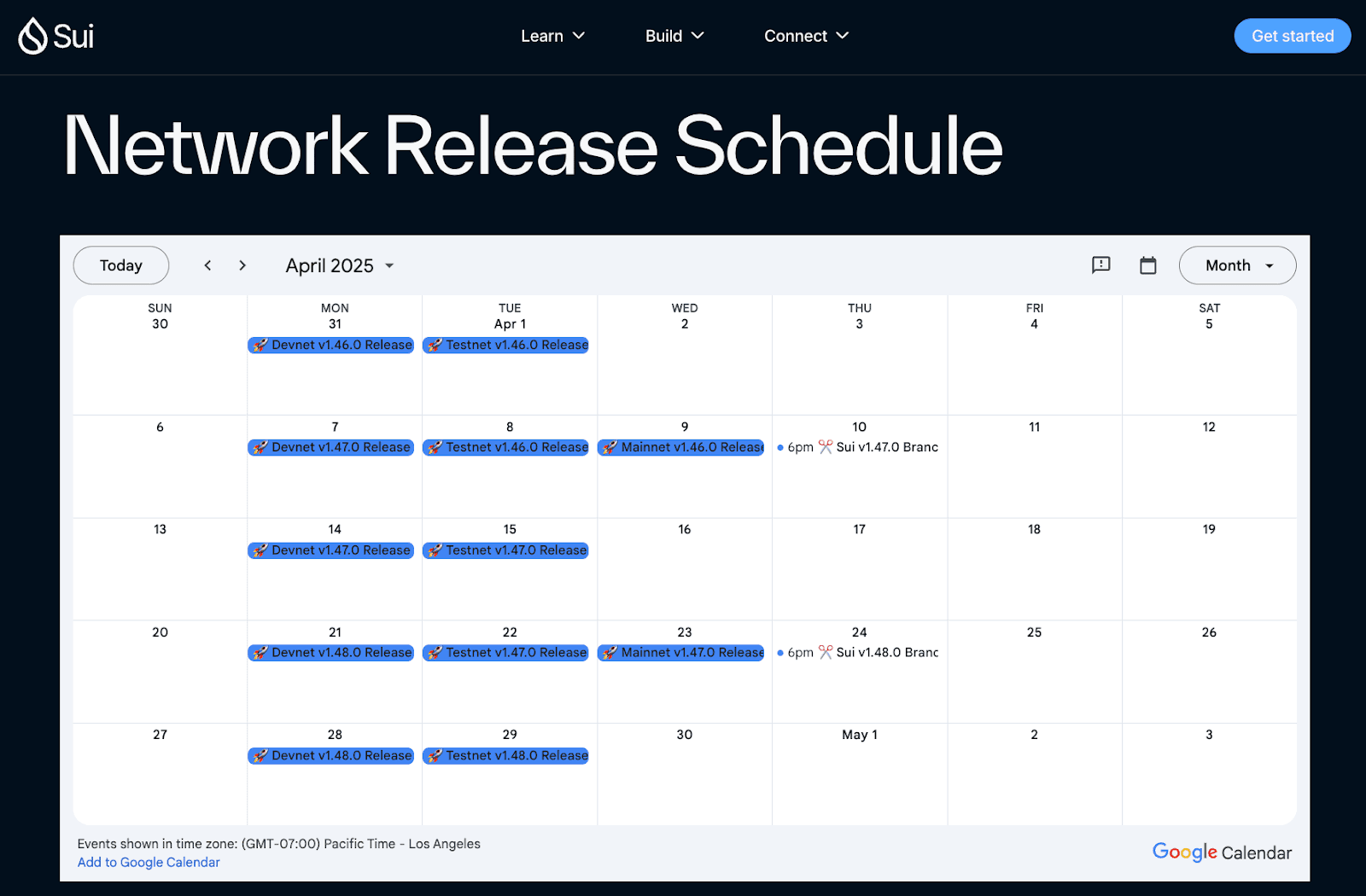

Frequent Releases

The most bullish thing I can say about Sui and the Mysten Labs team might be their implementation of a release calendar. With mainnet releases every two weeks, interspersed by testnet releases, this team ships.

Solana, by comparison, used to have a frequent, unscheduled pace of releases, until the numerous mainnet outages called the “move fast, break things” strategy into question.

Sui plows on at a steady, predictable pace. They are moving fast, and not breaking much.

From our side, it’s refreshing to know when to expect releases, instead of being on our toes for an upgrade on any day of the week. That being said, Sui’s shorter epochs (24 hours instead of ~56 hours on Solana) do leave less time for upgrades to be implemented, so a schedule also becomes more a necessity in Sui’s context.

V. Liquid Staking - Sui’s Biggest Missed Opportunity?

In my view, liquid staking is the biggest area for improvement on the Sui blockchain. Diving into each of the liquid staking protocols shows that they do not contribute to decentralization, rather the opposite. And with less than 2% of the supply liquid staked, they’re clearly not succeeding, despite an early 25M delegation from the Sui Foundation.

The liquid staking situation on Sui is a far cry from the performance-based auto delegation strategies of Solana’s staking pools, or Lido’s carefully constructed set of operators on Ethereum. It’s a real shame, because liquid staking has the potential to introduce new community-driven validators to the network, or create a better stake distribution across existing validators.

SpringSui: One Validator Only

A partner project of SuiLend, SpringSui has attracted 60M Sui of stake to its LST, sSUI, making it the largest liquid staking protocol. This is entirely staked to the SuiLend validator, which has almost 150M SUI staked, hosted by ServeTheWorld AS in Norway. Users therefore forgo any benefit of having stake spread across multiple validators, and the 60M of stake does little to help decentralize the network other than contribute to an already-large validator. (Although, the use of a unique hosting provider and location does merit some praise.)

Haedal: A Centralizing Pool

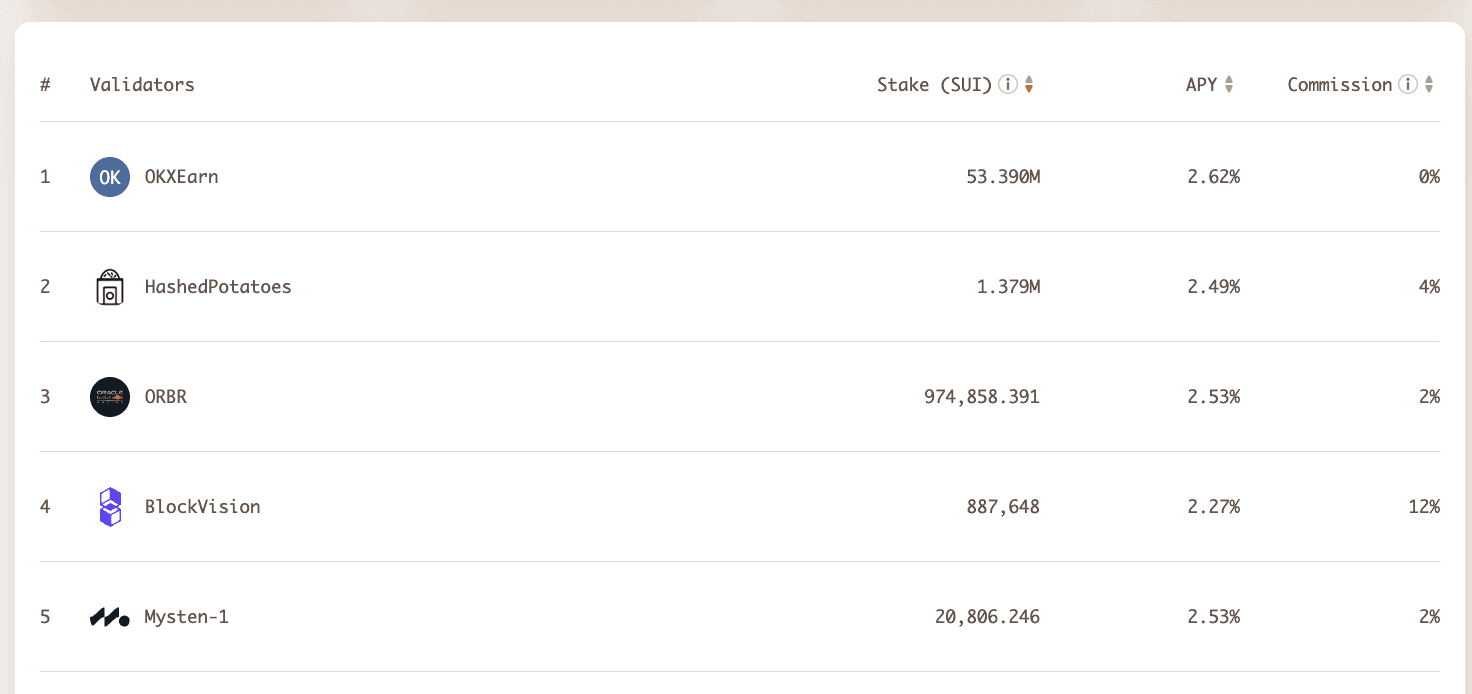

With 56M tokens staked, and a steady trend of growth, Haedal Protocol is Sui’s 2nd largest largest liquid staking protocol, and, sadly, the only pool that delegates stake to multiple validators. Unfortunately, it has the most bizarre delegation breakdown I’ve ever seen: as I write this, over 95% of their stake is delegated to the OKXEarn validator.

At first, I thought this couldn’t be correct, maybe there was an error in their website front-end. But after opening a ticket in their Discord, a team member confirmed:

“Because Haedal dynamically allocates to the highest-yielding validators, and currently OKX offers the highest yield with 0% commission, a large portion of the stake naturally flows to OKX.”

This is spelled out by their delegation strategy, which says

“We calculate the performance score of each validator at each epoch and re-balance stake based on the results. We plan to collect a variety of data for each validator (stake amount, commission, APY, block production, etc.) and use this data to calculate the score.”

There are seven other validators within 0.1% APY of the OKX validator, and an additional ten within 0.2%. Is the difference between 2.62% and 2.42% APY really worth the difference between delegating to one validator versus 18?

The fact that Sui’s largest liquid staking protocol delegates 95% of its stake to a single validator run by a centralized exchange, in the name of 0.2% APY increase for its stakers, seems both bizarre and a huge missed opportunity to contribute to the decentralization of the Sui blockchain. This is especially true in the context shared earlier, where the majority of validators currently depend on the Foundation to remain active.

By prioritizing APY, Haedal claims to take the staker-centric approach. However, what’s good for the Sui network is surely good for the SUI token, and thus good for Haedal’s stakers. Besides, with 95% of stake going to a single validator, stakers lose any benefit that could be had by distributing their stake across multiple validators. Haedal is in the midst of a token launch, and from my observations it seems their focus is on increasing the prevalence of their haSUI across DeFi. Maybe it’s possible to bring attention to their delegation strategy, and convince their community to re-asses their priorities. I’ll see what I can do.

Volo: Lack of Clarity

With 28.6M SUI staked, down from 60M, Sui’s second-largest liquid staking protocol has a severe lack of clarity around their delegation strategy. Their mainnet launch blog article says

"Volo depends on select node operators to stake pooled assets in a decentralized way.”

Their homepage shows the logos of 88 validators but offers no further context other than “Discover some of the most popular validators supporting the growth of Liquid Staking on SUI.” The only hint is buried in their docs, which say

“Our backend observes the network state and prioritizes validators based on their APY, reputation and already staked amount”.

To make matters more confusing, on their blog they announced a partnership with Luganodes, but no other operators. In a discord ticket, I was told “let me ask the team”, reflecting an equal lack of understanding by their admins and low-level employees.

Again, I see here a missed opportunity to make a tangible difference in the stake going to validators. If they are indeed spreading their 28.6M stake across 88 validators, they are unlikely to make a difference for any one validator in helping them become independent of Foundation stake. If they only stake with Luganodes, they further centralize the network and fail to pass multi-operator benefits to their stakers. But the lack of information provided leaves us all in the dark.

AftermathFi: One Validator

With 10M SUI staked, down from 33M, AftermathFi is the 3rd largest liquid staking protocol. Notice I didn’t call them a pool, because they run their own validator, hosted by OVH SAS in Germany. I totally support ecosystem projects running validators and gaining foundation stake to fund their development errors, but the strategy employed by Aftermath means that its stakers lose out on the benefit of having their stake distributed to multiple validators.

Also, the Aftermath validator has a massive stake of 154.7M SUI, 15x larger than the TVL of the liquid staking protocol, making it the 5th largest validator on the Sui network. It turns out that they were a genesis validator, with Sui Foundation undoubtedly staking a large amount in the hopes of funding development efforts for their staking protocol.

In reading a bit more, it seems Aftermath aims to create many more financial products than just liquid staking. It’s fair enough to fund their development with a highly-staked validator, but with over 2% of network stake on their validator, it reduces network decentralization instead of contributing to it. Another missed opportunity, in my opinion.

AlphaFi: One Validator

With 8.1M SUI staked in AlphaFi’s stSUI, AlphaFi is a relatively new protocol, but seems it might soon overtake Aftermath. Like Aftermath, the primary focus of AlphaFi is likewise not liquid staking but yield optimization, of which their liquid staking token plays a role. Also similar to Aftermath, AlphaFi runs their own validator, hosted by Latitude.sh in the US, with 37M of stake, 30M of which comes from the Foundation.

A Vision for Better Liquid Staking on Sui

I was quite disappointed by my research into liquid staking providers. By contrast, when I entered the Solana space in 2022, Marinade’s pool was automatically delegating stake to hundreds of operators based on a combination of performance and decentralization. Eventually Jito came along with their liquid staking pool, which focused on performance and currently allocates stake to the 200 top-ranked operators. Liquid staking pools such as these upheld decentralization as a key tenant, and significantly impacted the growth of Solana’s validator network. As the only validator in our data center, we were able to maintain profitability thanks to auto-delegated stake from Marinade and Jito, and the network benefited as a result.

With the current lack of attention to decentralization in Sui’s liquid staking marketplace, this could easily become a differentiator for a serious protocol to stand out from the crowd. Whether it will take a new protocol, or a shifting of priorities from existing protocols as they evolve, only time will tell. But I think it’s time to raise these concerns to the broader community and see if decentralization resonates as a theme.

VI. Conclusion

With 108 validators hosted by 36 providers in 22 countries, the decentralization of the Sui validator network is consistent with (or better than) other blockchains. With a Nakamoto coefficient of 18, stake distribution is heavily influenced by Sui Foundation but is reasonable overall, despite the two largest validators being run by Mysten Labs.

The barrier to entry for new validators is significant, requiring server-grade hardware and over $50M of SUI tokens to become active on the network. The Foundation makes up the majority of delegated stake for many validators, effectively holding the power to remove validators from the network.

That being said, the Foundation deserves praise for bootstrapping a network of 100 validators, instead of launching with a much smaller number, as we’ve seen on too many recent network launches. Not only that, but the rapid release schedule for new validator client versions, and their transparent and responsible handling of bugs and vulnerabilities is exemplary.

Despite launching with only 5% of circulating supply, token inflation remains under control thanks to an ever-decreasing staking APY, now below 2.5%. Despite the low APY, over 75% of tokens staked create $20B of economic security for the Sui blockchain.

Overall, at H2O Nodes we’ve had nothing but positive experiences working with Mysten Labs and Sui Foundation. Their people are smart, they ship, and their software works. In the node operator business, this is a breath of fresh air.

As evidenced by our participation in the recent launch of the Walrus mainnet, and our investment in Ika and participation in their testnets, we are very bullish on the entire Sui ecosystem and expect great things. That being said, we do believe that decentralization is a neverending journey, and I hope that content like this which increases transparency around the state of the network can inspire efforts to make it even better.